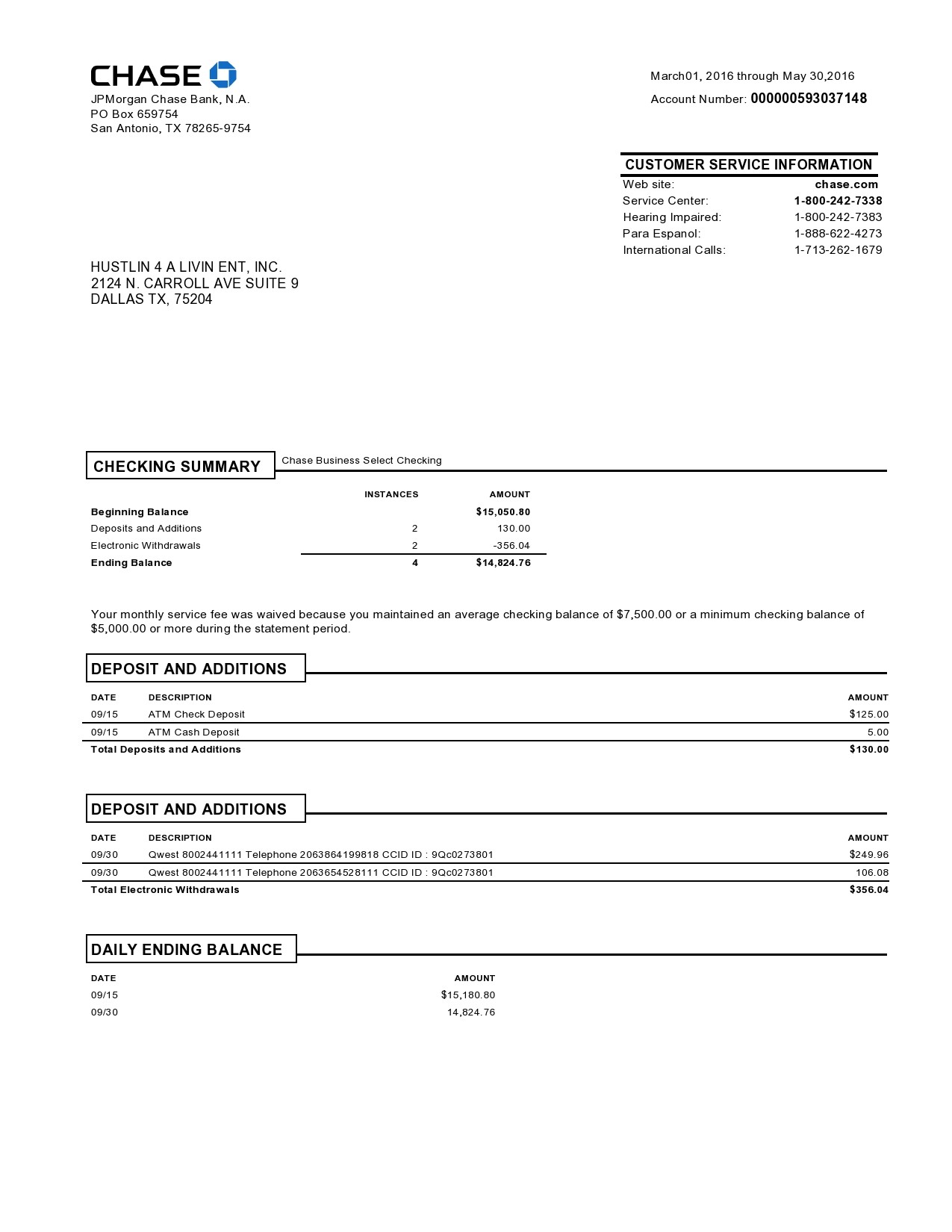

Chase Mortgage Interest Statement: A Comprehensive Guide You Need To Read

Hey there, folks! If you're reading this, chances are you've been scratching your head over that Chase mortgage interest statement thing. Don't worry, we've got you covered. Whether you're a first-time homeowner or a seasoned property owner, understanding your mortgage interest statement can feel like solving a complex puzzle. But guess what? We're here to break it down for you in simple, easy-to-understand terms. So, let's dive right in and make sense of that Chase mortgage interest statement once and for all!

Let's face it, buying a house is one of the biggest financial decisions you'll ever make. And once you sign on that dotted line, you're handed a pile of paperwork, including that infamous Chase mortgage interest statement. It's easy to get overwhelmed, but trust us, it's not as scary as it seems. This guide will walk you through everything you need to know about your mortgage interest statement and why it's such a big deal.

Now, before we get into the nitty-gritty, let's clear the air. A mortgage interest statement isn't just some random document your bank sends you. It's an essential tool that helps you track your payments, understand your tax deductions, and keep your finances in check. So, buckle up, because we're about to demystify the world of Chase mortgage interest statements together!

- Is Shaq Married The Untold Story Behind The Big Diesels Love Life

- Jackerman Video The Ultimate Guide To Mastering The Viral Sensation

What Exactly is a Chase Mortgage Interest Statement?

Alright, let's start with the basics. A Chase mortgage interest statement, also known as Form 1098, is essentially a record of the interest you've paid on your mortgage throughout the year. It's like a financial report card that summarizes your mortgage payments, including principal, interest, and any additional charges. This document is super important because it helps you when tax season rolls around.

For instance, if you've paid a significant amount of interest on your mortgage, you might qualify for some sweet tax deductions. The IRS allows homeowners to deduct mortgage interest from their taxable income, which can save you a pretty penny. So, yeah, your Chase mortgage interest statement isn't just a piece of paper—it's a key to unlocking potential tax savings!

Why Should You Care About Your Chase Mortgage Interest Statement?

Here's the deal: understanding your Chase mortgage interest statement isn't just about keeping records. It's about maximizing your financial health. By staying on top of your mortgage payments and knowing how much interest you've paid, you can make smarter financial decisions. For example, if you notice that your interest payments are through the roof, you might consider refinancing your mortgage to secure a better rate.

- Did Dwayne Johnson Die Debunking The Rumors And Celebrating The Rock

- Michael Cimino Actor The Man Behind The Lens And Beyond The Spotlight

Additionally, your Chase mortgage interest statement plays a crucial role during tax season. It's one of the documents you'll need to file your taxes accurately. Without it, you might miss out on valuable deductions that could save you money. So, yeah, it's kind of a big deal.

How to Read Your Chase Mortgage Interest Statement

Now that you know what a Chase mortgage interest statement is, let's talk about how to read it. At first glance, it might look like a bunch of numbers and codes, but once you break it down, it's pretty straightforward. Here are the key components you need to pay attention to:

- Loan Number: This is the unique identifier for your mortgage loan. It helps Chase keep track of your account.

- Mortgage Interest Paid: This is the total amount of interest you've paid on your mortgage during the year. It's the number you'll need for your tax deductions.

- Real Estate Taxes: If you've paid property taxes through your mortgage escrow account, they'll be listed here.

- Mortgage Insurance Premiums: If you're required to pay mortgage insurance, the premiums will be detailed in this section.

By familiarizing yourself with these components, you'll be able to make sense of your Chase mortgage interest statement in no time.

Common Mistakes to Avoid When Reading Your Statement

While reading your Chase mortgage interest statement might seem simple, there are a few common pitfalls to watch out for. One of the biggest mistakes people make is overlooking the fine print. Sometimes, additional fees or charges might be hidden in the details, so it's essential to read the entire document carefully.

Another common error is assuming that the mortgage interest paid is the same as your total mortgage payment. Remember, your monthly mortgage payment includes both principal and interest, so the interest amount will always be lower than your total payment. Don't let this discrepancy confuse you!

How Chase Mortgage Interest Statements Impact Your Taxes

Taxes, taxes, taxes—let's talk about how your Chase mortgage interest statement affects your tax return. As we mentioned earlier, the IRS allows homeowners to deduct mortgage interest from their taxable income. This deduction can significantly reduce the amount of taxes you owe, especially if you've paid a substantial amount of interest on your mortgage.

However, there are some rules you need to follow. For instance, the mortgage must be secured by your primary residence or a second home. Additionally, the loan amount must meet certain limits set by the IRS. If you're unsure about whether you qualify for the deduction, consult with a tax professional or accountant.

Tips for Maximizing Your Tax Deductions

Here are a few tips to help you make the most of your Chase mortgage interest statement during tax season:

- Keep Records: Always keep a copy of your Chase mortgage interest statement in a safe place. You never know when you might need it in the future.

- Double-Check Numbers: Before filing your taxes, double-check the numbers on your statement to ensure they match your records.

- Consult a Professional: If you're unsure about anything, don't hesitate to consult with a tax professional. They can help you navigate the complexities of mortgage interest deductions.

By following these tips, you'll be well on your way to maximizing your tax savings.

Understanding Mortgage Interest Rates

Let's take a quick detour and talk about mortgage interest rates. Your Chase mortgage interest statement reflects the interest rate on your loan, which is determined by several factors, including your credit score, the type of loan, and current market conditions.

Interest rates can fluctuate over time, so it's important to stay informed. If you notice that rates have dropped significantly since you took out your mortgage, you might consider refinancing to secure a lower rate. This could save you thousands of dollars over the life of your loan.

Fixed vs. Adjustable Rate Mortgages

When it comes to mortgage interest rates, you have two main options: fixed-rate and adjustable-rate mortgages. A fixed-rate mortgage means your interest rate stays the same for the entire term of the loan. This provides stability and predictability, which many homeowners prefer.

On the other hand, an adjustable-rate mortgage (ARM) has an interest rate that can change over time. This can be beneficial if rates are low when you take out the loan, but it also comes with some risk if rates rise in the future. Understanding the difference between these two types of mortgages can help you make an informed decision about your Chase mortgage interest statement.

How to Dispute Errors on Your Chase Mortgage Interest Statement

Mistakes happen, even with something as important as your Chase mortgage interest statement. If you notice an error on your statement, don't panic. There are steps you can take to dispute it and get it corrected.

First, gather all your documentation and compare it to the statement. If you find a discrepancy, contact Chase customer service and explain the issue. They should be able to investigate and correct the error. It's crucial to address any issues promptly, especially if the mistake affects your tax return.

What to Do If Chase Can't Resolve the Issue

In rare cases, Chase might not be able to resolve the issue to your satisfaction. If this happens, you can escalate the matter by filing a complaint with the Consumer Financial Protection Bureau (CFPB). The CFPB is a government agency that helps consumers resolve disputes with financial institutions.

Remember, your Chase mortgage interest statement is an important financial document, and accuracy is key. Don't hesitate to take action if you notice any errors.

Strategies for Reducing Your Mortgage Interest Payments

Let's face it, nobody likes paying interest. While it's an unavoidable part of owning a home, there are strategies you can use to reduce your mortgage interest payments. Here are a few ideas:

- Make Extra Payments: By paying a little extra each month, you can reduce the principal balance on your mortgage, which in turn lowers your interest payments over time.

- Refinance Your Loan: If interest rates have dropped since you took out your mortgage, refinancing could secure you a lower rate and save you money.

- Switch to a Shorter Loan Term: A 15-year mortgage typically has a lower interest rate than a 30-year mortgage. If you can afford the higher monthly payments, this could be a great option.

By implementing these strategies, you can take control of your mortgage and reduce the amount of interest you pay over the life of the loan.

The Benefits of Paying Down Your Mortgage Faster

Paying down your mortgage faster has numerous benefits. Not only will you save money on interest, but you'll also build equity in your home more quickly. This can be a huge advantage if you ever decide to sell your property or take out a home equity loan.

Plus, there's something incredibly satisfying about owning your home outright. It's a sense of financial freedom that many homeowners strive for. So, if you have the means, consider accelerating your mortgage payments and enjoy the long-term benefits.

Final Thoughts and Call to Action

Well, there you have it—a comprehensive guide to Chase mortgage interest statements. We hope this article has helped demystify the process and given you the tools you need to take control of your mortgage. Remember, understanding your Chase mortgage interest statement is key to maximizing your financial health and taking advantage of valuable tax deductions.

Now, it's your turn to take action. If you have any questions or need further clarification, don't hesitate to leave a comment below. And if you found this article helpful, be sure to share it with your friends and family. Together, we can empower homeowners everywhere to make smarter financial decisions!

Thanks for reading, and happy homeownership!

Table of Contents

- What Exactly is a Chase Mortgage Interest Statement?

- Why Should You Care About Your Chase Mortgage Interest Statement?

- How to Read Your Chase Mortgage Interest Statement

- How Chase Mortgage Interest Statements Impact Your Taxes

- Understanding Mortgage Interest Rates

- How to Dispute Errors on Your Chase Mortgage Interest Statement

- Strategies for Reducing Your Mortgage Interest Payments

- Final Thoughts and Call to Action

- Seinfeld Height The Inside Scoop On Tvs Favorite Comedian

- Samantha Middleton Husband The Untold Story You Wonrsquot Believe

Mortgage Settlement Statement How to create a Mortgage Settlement

Chase Bank Statement Template Chase Total Checking MbcVirtual in

Chase Bank Statement Template